![]()

This article appears in Charlotte Business Journal.

Unraveling the Mysteries of Medicare

As we enter the 2024 Medicare open enrollment period (October 15, 2023, to December 7, 2023), we are helping break down some of the complexities of Medicare. At age 65, Medicare, the U.S. government’s health care system for seniors, is likely to appear at the top of your to-do list. We hope this is a helpful summary and as always, we are here to answer any questions and refer you to our expert resources if needed. To start, you’re probably asking yourself questions like:

- What should I do about Medicare?

- When is the best time to enroll in Medicare?

- Should I choose traditional Medicare or Medicare Advantage?

- If I choose traditional Medicare, do I need Medicare Supplement (MedSupp) or a Medigap policy?

- Which Medicare Supplement plan is right for me?

Medicare Breakdown

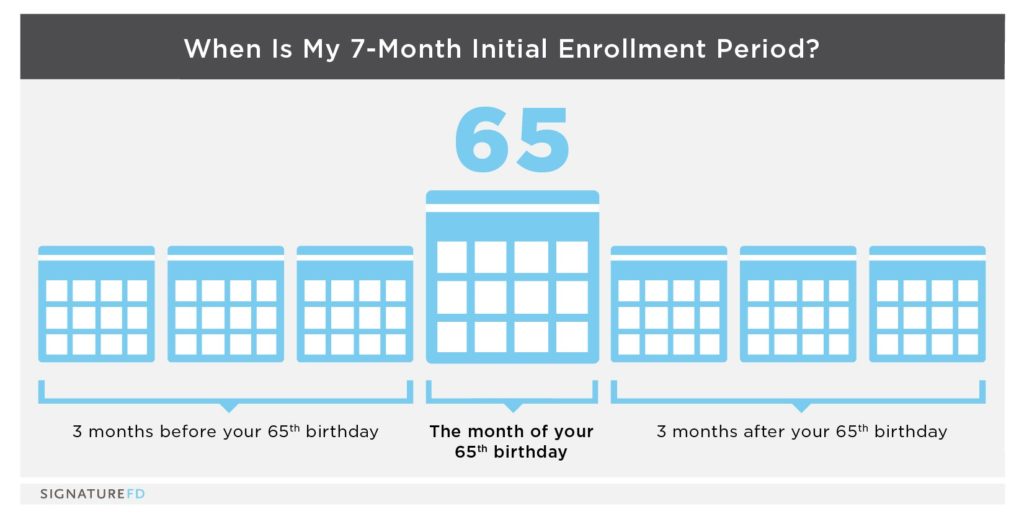

With certain exceptions, we are all required to enroll in Medicare within a seven-month period that centers around your 65th birthday. The enrollment period begins three months prior to the month of your 65th birthday. Failure to enroll when required can lead to penalties that increase Medicare premiums for life.

THE 8 STEPS TO FINANCIAL READINESS

Make the most of your wealth now and in the future while assessing challenges, opportunities, and risks along the way. That way, you can grow, protect, give, and live your wealth in a way that aligns with what matters most: your Net Worthwhile™.

THE 8 STEPS TO FINANCIAL READINESS

Make the most of your wealth now and in the future while assessing challenges, opportunities, and risks along the way. That way, you can grow, protect, give, and live your wealth in a way that aligns with what matters most: your Net Worthwhile™.

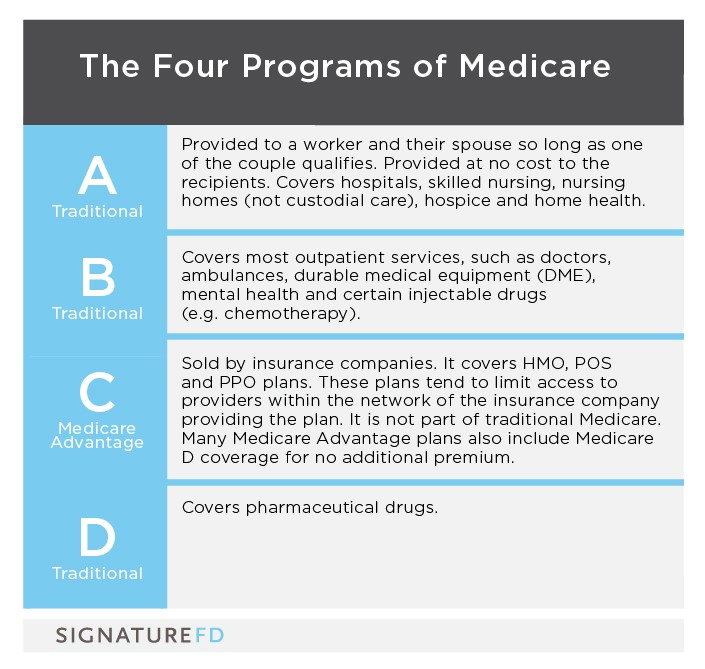

There are four parts to Medicare: A, B, C and D, along with Medicare Supplement policies. Medicare A and B are provided by the government. Medicare C and D and Medicare Supplement insurance are sold by private insurance companies.

With traditional Medicare, A, B and D are required (unless you have qualifying alternative coverage), while the Medicare Supplement Policy is optional. Medicare Supplement policies pay expenses that are not paid by Medicare A and B, such as deductibles, co-pays and co-insurance. Medicare C, also known as Medicare Advantage, includes comprehensive coverage that can replace Medicare A and B, as well as Medicare Supplement. Some Medicare C policies can also replace Medicare D. One significant drawback to Medicare C, for some clients, is that the network of providers tends to be more limited and less flexible than with traditional Medicare.

Medicare B and D Premium Adjustments

Medicare B and D premiums may include an addition to the base premium that is based on income — with higher incomes equating to higher premiums. This amount is referred to as the Income Related Monthly Adjustment Amount (IRMAA). IRMAA for Medicare is based on Modified Adjusted Gross Income (MAGI).

MAGI = AGI* + Tax-Exempt Interest

* AGI, or adjusted gross income, can be found on line 11 of Form 1040 in your 2022 tax return.

The MAGI of two years prior determines Medicare premiums in the current year. For example, the applicable MAGI to determine your Medicare premiums for 2024 will be determined from your tax return for 2022. Depending on your income, your monthly Medicare B premium for 2024 can vary within a range. Permanent late enrollment penalties may also apply.

Access more information (Note: This has not yet been updated for the 2024 enrollment period, but can give you an idea of how IRMAA and the brackets work). Medicare D premiums vary widely depending on the insurance company and drugs offered. These premiums may also have an IRMAA depending on your MAGI.

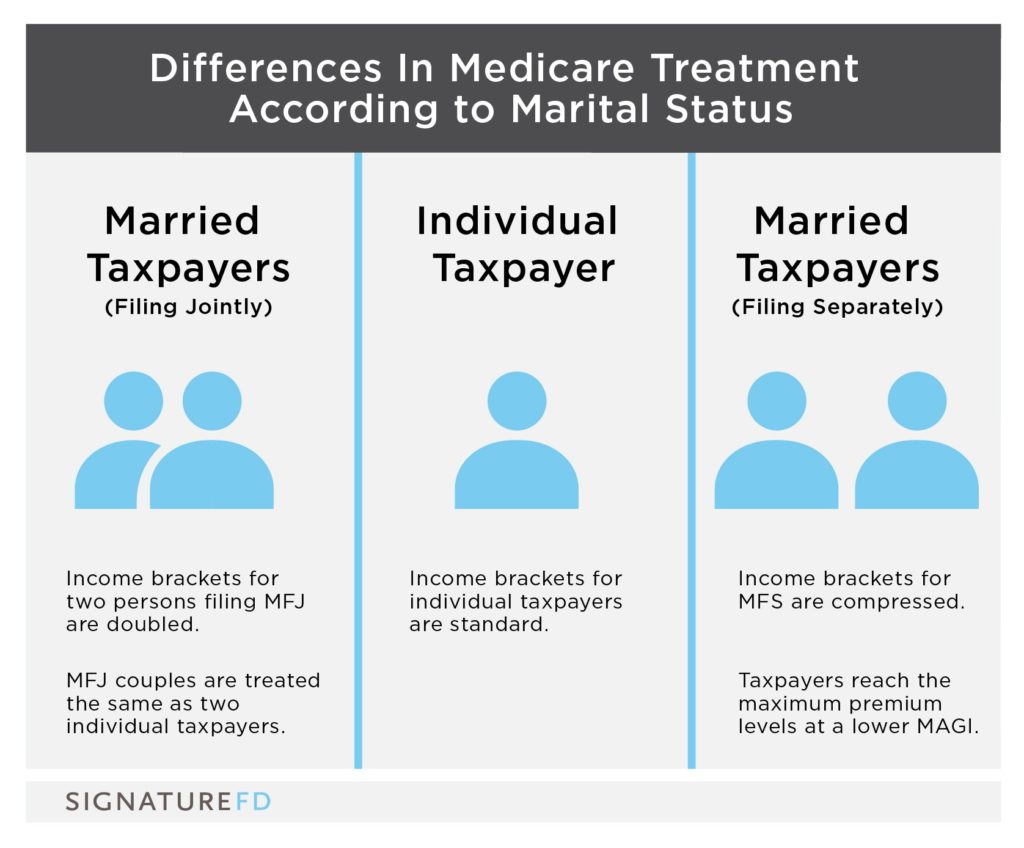

Taxpayers enroll in Medicare as individuals, whether they file tax returns as single, married filing jointly (MFJ), or as married filing separately (MFS). Means testing income brackets for persons who file as MFJ are doubled compared to the brackets for single filers. This structure ensures comparable costs per person. However, married filing separately income brackets are compressed. As a result, MFS filers reach maximum premium levels more quickly.

Medicare policies have several limitations compared to standard insurance coverage. Medicare does not cover vision, dental care, hearing aids, routine podiatry and long-term care. Importantly, Medicare does not have limits on annual or lifetime liability. Liability is unlimited. Medicare does include deductibles, co-pays and co-insurance.

Medicare Supplement Insurance

Limitations of the traditional Medicare programs A and B left many seniors exposed to financial risk. In response, the government designed Medicare Supplement Insurance, called MedSupp or Medigap plans, which are sold by insurance companies. The various Medicare Supplement policies are identified by letters: A, B, *C, D, G, K, L, M, N. Medicare Supplement plans cover some or all the deductibles, co-pays and co-insurance related to Medicare A and B, as well as out-of-pocket expenses of unlimited liability. However, as of January 1, 2020, Medigap policies sold to new Medicare enrollees will not cover the Part B deductible. As a result, *Medigap plan C is now unavailable for new enrollees. If you were enrolled in plan C before January 1, 2020, you may keep your coverage.

In terms of coverage, one of the most comprehensive Medicare Supplement policies is Plan G, which is frequently selected by SignatureFD clients. It covers most Medicare deductibles, co-pays and co-insurance. Before selecting a plan, please review each supplement to determine which is right for you. Discounts may be available for spouses who are purchasing plans from the same insurance company. The plan premium and discount depend on the carrier and plan selected.

Determining Your Cost of Medicare

The Medicare premium brackets and costs have not yet been released for 2024. However, once costs are released, they can be found at medicare.gov/basics/costs/medicare-costs. Use the tables and your 2022 tax return to estimate your 2024 traditional Medicare premiums. To determine which bracket you are in, calculate your modified adjusted gross income (MAGI) as mentioned above. Medicare A is at no cost for individuals who qualify for Medicare. The total cost will be your Medicare Part B cost, the cost of your Medicare Part D and the cost of your Medicare Supplement policy. This should be a rough estimate for your premium expenses associated with Medicare.

There are other Medicare complexities beyond the scope of this article. However, this can help you start to work through some of the mysteries surrounding Medicare. If you have questions about Medicare or need help enrolling, please contact your SignatureFD relationship manager. We work with an external resource that we feel confident can help answer questions and help take the mystery out of the enrollment process. For additional resources, including the Medicare Eligibility & Premium Calculator, you can also visit medicare.gov.

Do you need assistance understanding Medicare premiums, brackets and enrollment options? Contact Vicki Shackley, director of SignatureWOMEN®, today.

SignatureFD is a financial advising firm headquartered in Atlanta, Georgia. We believe in helping our clients achieve wealth beyond money. Our team of investment and financial planning experts are committed to proactively helping clients take control of their financial lives and achieve their goals.

Vicki Shackley, JD, LLM, CFP®, is a partner, wealth advisor and director of SignatureWOMEN®. Shackley is a former estate planning attorney with a Juris Doctorate and Master of Law in Taxation. She is a member of the Florida Bar Association and the Financial Planning Association of Georgia.

THE 8 STEPS TO FINANCIAL READINESS

Make the most of your wealth now and in the future while assessing challenges, opportunities, and risks along the way. That way, you can grow, protect, give, and live your wealth in a way that aligns with what matters most: your Net Worthwhile™.

THE 8 STEPS TO FINANCIAL READINESS

Make the most of your wealth now and in the future while assessing challenges, opportunities, and risks along the way. That way, you can grow, protect, give, and live your wealth in a way that aligns with what matters most: your Net Worthwhile™.